Public sector pensions in Newfoundland and Labrador are underfunded. There’s not enough money in the fund account to cover all the likely money they’d have to pay out to people when they retire.

But make no mistake, the province’s public sector pensioners are not in any real danger of losing their pensions as a result. That’s because the Pension Fund Act guarantees that the provincial government will make up any difference between the money owed to pensioners annually and the money available from the fund. Unless some provincial government in the years ahead changes the law governing the pensions, people will get the money and benefits they’ve been promised.

The provincial government isn’t going to default on pensions any more than they are likely to take the completely irresponsible advice some might give them to change all the plans immediately - unilaterally if necessary - to make them defined contribution plans instead of defined benefit plans.

It’s important that people remember that because there is a concerted effort going on at the moment to mislead people about public sector spending generally, and pensions in particular.

The Pension Problem in Perspective

Some groups, like the Canadian Federation of Independent Business, want to gut the existing pension and retirement benefits plan for firefighters and police officers in Newfoundland and Labrador, for example. They want to replace then with something they describe as “affordable” pension plans.

The CFIB and others involved in the attack on public sector pensions will use all sorts of code words and phrases to describe their idea but what it boils down to is simple: firefighters and police officers in the future would not get anything but a tiny fraction of the retirement and pension benefits their current work agreements commit us all to providing them.

The firefighters, corrections officers, and police officers are a good example of public sector pensions in the province. These people provide a vital public service. It is tough and dangerous. Police officers and firefighters risk their lives every day on the job.

And yet the CFIB thinks that their pensions need to be slashed. Unaffordable, they say. Too rich. Unfair to taxpayers, who include, incidentally, the firefighters, corrections officers, and police officers.

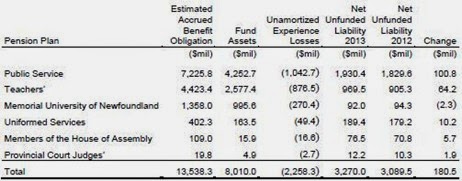

The truth is that the Uniformed Services Pension Plan fund in Newfoundland and Labrador is short $190 million. There’s another $50 million in experiential loss we need to find because the investments that feed the fund made less money than forecast. Give them another six percent of the unfunded health and life insurance benefits liability because that’s roughly the size of the uniformed service pension plan relative to the other public sector plans.

That adds up to $420 million.

That’s it.

Let’s put that in perspective.

The current provincial budget deficit in the Estimates is $1.3 billion or roughly three times that much. In other words if the provincial government budget works out exactly as forecast, they would have to borrow $1.3 billion in cash just to make ends meet. The government is spending that much more than it can afford in the current budget.

Look at it another way. The provincial government in Newfoundland and Labrador will spend the most per person of any provincial government in Canada to deliver services to the public. This province spends more than Alberta, more than Saskatchewan, and more than Prince Edward Island.

Sounds crazy, but it is true. And it has been true for a very long time, long before this became a “have” province. The Royal Bank’s economics section has a neat comparison of the cost per person to deliver services in every province of Canada, over time. More people should read it.

So we know the provincial government is spending more than it takes in and has been doing that for some time. That’s the text-book definition of unaffordable. If the “have” provincial government in Newfoundland and Labrador spent the same per person as Alberta – wealthy old Alberta – the provincial government would spend $2,038 per person less than the current forecast.

If we allow there are roughly 520,000 people in the province, that works out to about $1.059 billion on a budget of around $8.0 billion. That’s a little more than twice the amount we owe to the pension fund for firefighters, warders, and police. It’s also enough such that - with a bit of work - you could cover the entire unfunded pension liability for everyone, including the so-called experiential losses in less than a decade.

It wouldn’t be easy. But it would be attainable. Doable.

Some public servants would lose their jobs if we cut spending by that sort of amount. But then again, the main reason we have such a huge unfunded pension liability is that the provincial government added huge numbers of public servants after 2006 and also boosted their pay.

But basically, you can see that while the pensions are underfunded, they are most certainly not unaffordable. In fact, the provincial government could have knocked off pretty much the entire unfunded liability in 2007 or so out of a single year’s worth of oil money. That’s not necessarily what they should have done, in one swoop, but those figures give you a pretty good idea that the people claiming the current pension plans are unaffordable aren’t talking about what is actually going on in this province.

And since the unfunded pension liability is a fraction of the enormous public debt debt – around $18 billion at least – these days, the provincial government is going to have to do something to get its spending under control anyway. Pensions are just part of a much bigger problem.

The bond-rating agencies have warned the government about its public debt in the past decade, and that was before the current administration raised the debt with the first instalment - $5.0 billion - of the Muskrat Falls debt. We don’t know how much the total will be beyond $5.0 billion. We just know that it is going to be way more than five.

Skewed Perspective of Special Interest Groups

With that in mind, let’s widen our perspective here. What does the CFIB think about the provincial government’s massive deficit budget?

“CFIB is pleased with the Budget [2014]….”

Huh?

Doesn’t make sense, does it?

Continued overspending. Massive increase in the debt. No real sign of any improvement in that situation.

CFIB is happy.

That’s not surprising, really. Special interest groups like CFIB, the board of trade, and their like seldom give sound public policy advice. They aren't interested in broader public issues. They want to look after their members, in the CFIB case, some small business owners who – as it seems – are perpetually concerned to cut taxes. Doesn’t matter what the issue. CFIB wants to slash taxes.

Interestingly, though, they aren’t concerned with government overspending that will lead to high taxes and, in one case lead to a massive new tax called Muskrat Falls. The CFIB thinks that borrowing a billion dollars in 2014 (it could well be more than that) is okay because it is for “short-term infrastructure expenses” for things like Muskrat Falls. That’s what the CFIB called it.

The current plan for Muskrat Falls is to tax people in the province – including businesses - to pay all of the cost for Muskrat Falls, plus profit for large businesses like Emera. The term of the debt is 30 years, at least, and officially 50 years. That’s not short-term by any stretch of anyone’s imagination. And for the next decade or so, the provincial government and Nalcor will be borrowing and borrowing to pay for it.

CFIB is happy with that sort of spending because its members stand to benefit.

D’uh.

If CFIB was genuinely concerned about “affordable” public spending and cutting debt, they couldn’t possibly justify a massive increase in public debt coupled with the enormous tax hike it is going to take to pay for it. and the rest. And yet they do. That’s because the CFIB is just another special interest group that wants public money for itself. And in their lobbying, they practice decision-based evidence making. Their arguments cherry-pick information to support predetermined conclusions.

Don’t hate special interest groups for what they are. Just understand them. They have a part to play in our political system. Just remember that the genuine public interest isn’t on their agenda any more than it’s on the agenda of any other special interest group. Someone else gets to figure that out, namely voters and the politicians the voters elect to run things. Chide special interest groups for their BS – it can be loads of fun - but understand what they are and what they are doing.

No one is going to do anything rashly

Let’s get back to the public debt and pensions.

The provincial government isn’t about to default on their pension obligations. They aren’t going to let the funds go bankrupt, nor are they going to step in and unilaterally shift anything around.

The reason is pretty simple: pensioners are government creditors. If government unilaterally changed its obligations to pensioners to give the pensioners less than they currently are owed, it would be pretty much the same as unilaterally restructuring government’s bank loans or bonds. Bondholders, banks, and other creditors not to mention bond rating companies don’t like that sort of thing. They are a bit funny about getting screwed out of the money people owe them.

If government borrowed $100 million dollars at five percent interest for 30 years, for example, the people who loaned the money expect to get paid in full, on time. Period. And the government ordinarily wouldn’t decide one day to tell the bank: screw you, we aren’t paying you a penny more than we have already.

Things would have to be pretty extreme for government to flip its creditors the middle finger. Think Iceland a couple of years ago or Newfoundland in the 1930s. We aren’t there yet, but make no mistake: extreme action to deal with public sector pensions of the kind some are advocating would send a very powerful and very bad message to creditors about the state of the provincial government’s finances.

Nothing would create a political and financial crisis for a province like taking such radical action as defaulting on a debt or unilaterally changing the government’s commitment to 70,000 taxpayers who are effectively creditors. The people to whom government owes big money will get the unmistakeable message that the government finances are in a Greek-like mess.

Investors get nervous when things like that happen. They tend to pull their money out. So even if someone thought that default or unilateral restructuring of debts would fix a crisis, the reality is that the dramatic action would guarantee that something that might only look like a crisis became a very real one in a big hurry.

That doesn’t mean the provincial government in Newfoundland and Labrador doesn’t have a serious debt problem to deal with. It does. Regular SRBP readers know that the provincial debt is a huge concern around these parts. The only thing of greater concern than the debt itself is the fact that everyone keeps talking about it but no one does anything but make it that much bigger, again.

Nor does it mean that the bond ratings agencies – Moody’s, Standard and Poors, and Dominion Bond Rating Service - haven’t noted concern about some part of the province’s debt load in any of the their reviews over the past year. They have. One part of the debt isn’t a problem: the whole debt is a problem.

The Lowest Common Denominator

Still, the provincial has yet to do anything to reduce debt in a significant way or deal with parts of the public debt like the unfunded pension liability. The reason is simple and political.

For one thing, there’s no agreement among the politicians about what to do. Over the past decade, for example, the provincial Conservatives have talked a lot about reducing debt and tackling the unfunded pension liability. Tom Marshall has been at the centre of power in the province for a decade and still he can’t seem to get people to do anything about the public debt.

That’s because Marshall thinks debt is an issue like his predecessor as finance minister - Loyola Sullivan - thought it was a problem. Others disagree, just like they dismiss demographic change as irrelevant because it doesn’t fit with their preconceived ideas or their own political interest. The result is that nothing happens to the debt.

The second reason for government inaction on debt is also political. If the provincial government fixed the public sector pensions by doing what they need to do – put more money into the plans – then the government would make the pensioners happy.

And that’s all they’d do.

If – on the other hand – the provincial government took all that money and spent it, they’d stand to make lots of people happy. Not surprisingly, that’s what the government has usually done. The Conservatives are just the latest version of the same basic way of political thinking in Newfoundland and Labrador.

Rather than look after the pension liability or control public spending, they hired thousands of people and increased their salaries to boot. They jacked up government spending to record heights and made the unfunded pension liability far worse than it was. Everybody loved them at the polls.

There’s no small measure of hypocrisy, either, that the same business groups who today are leading the ideological assault on public sector pensions, had no problem with government mismanagement that drove up public debt and guaranteed huge subsidies to the private sector at taxpayer expense.

The St. John’s Board of Trade, for example, the same people who can’t explain what public debt is, had no problem loving up budget after overspending budget. They also gleefully endorsed $8.0 billion in new public debt from Muskrat Falls and what amounts to a $450 million new tax on local taxpayers so that the provincial energy company can sell discount electricity to Nova Scotia-based Emera and to multi-billion dollar multi-national mining companies in Labrador.

Yet in 2014, the Board of Trade is part of an attack on unfunded liabilities for public sector pensions that went unaddressed as government overspent annually with the full support of groups like the Board of Trade and the Canadian Federation of Independent Business.

Making Things Right

What you can see - pretty plainly in fact – is that lowest denominator politics unites politicians and special interest groups in a perfectly understandable way. Changing that will be very difficult. It will take a very special set of circumstances or a very special politician or group of politicians to bring about such a fundamental change in provincial politics that they might actually get provincial government spending under control.

Even if no politicians or special interest groups are actually talking about changing public policy on debt and public spending doesn;t mean we should talk about it. To the contrary, we will never make a change if we lose sight of the desired change altogether. We must keep looking at the issue and the options. One day, things will change.

Because public debt and overall public spending are intertwined, you really can’t deal with one without dealing with the other. Overspending – so ingrained in our political culture – just drives up public indebtedness. Today, the provincial government collects more money than at any time in its history and yet overspends to the point where government plans to increase an already enormous public debt. If you reduce debt, you merely give the over-spenders more room to overspend.

That’s why the only sensible solution to the province’s public debt problem is one along the lines of the SIDI model that SRBP proposed last spring. You’ve got to have a spending control policy including infrastructure spending, a debt reduction policy, and an investment policy to bring in new cash. All three elements work together.

The SIDI simulation included:

- a steady, sustainable increase in spending each year,

- an unprecedented, sustainable capital works program,

- a $3.675 billion real decrease in public debt,

- the prospect of a complete elimination of public debt within a decade, and,

- an income fund that would continue to grow with further oil money and generate new income for the provincial government for as long as the fund existed.

Until politicians start talking about those types of ideas or until taxpayers start demanding them, we won’t get any government financial policy that is genuinely in the long-term public interest.

What we will get are special interest groups who focus on their own interests alone. Listening to one special interest group or another won’t produce a solution that is in the public interest, that is genuinely fair and balanced.

You see, no one who is genuinely concerned with the public good of Newfoundlanders and Labradorians would advocate gutting pensions for firefighters, police, corrections officers, nurses, restaurant inspectors, social workers, and a host of other valuable public servants when the provincial government already has the money to fund their existing pension plans fully.

-srbp-